Delhivery Ltd’s shares are hovering near their 52-week lows of ₹325.50 apiece seen on 18 November. Investor sentiment remains subdued given the uninspiring September quarter (Q2FY25) results amid rapid growth in quick commerce and stiff competition in e-commerce. Further, the rise of in-house delivery fleets by e-commerce giants such as Meesho has added to the pressure.

Delhivery’s management is confident that the worst of the express parcel insourcing trend is now behind them. Demand conditions in H1FY25 were muted, especially in the express parcel segment, partly due to seasonality as Q2 is usually a softer quarter. But signs of recovery are emerging. The festive season volumes were up 30% year-on-year.

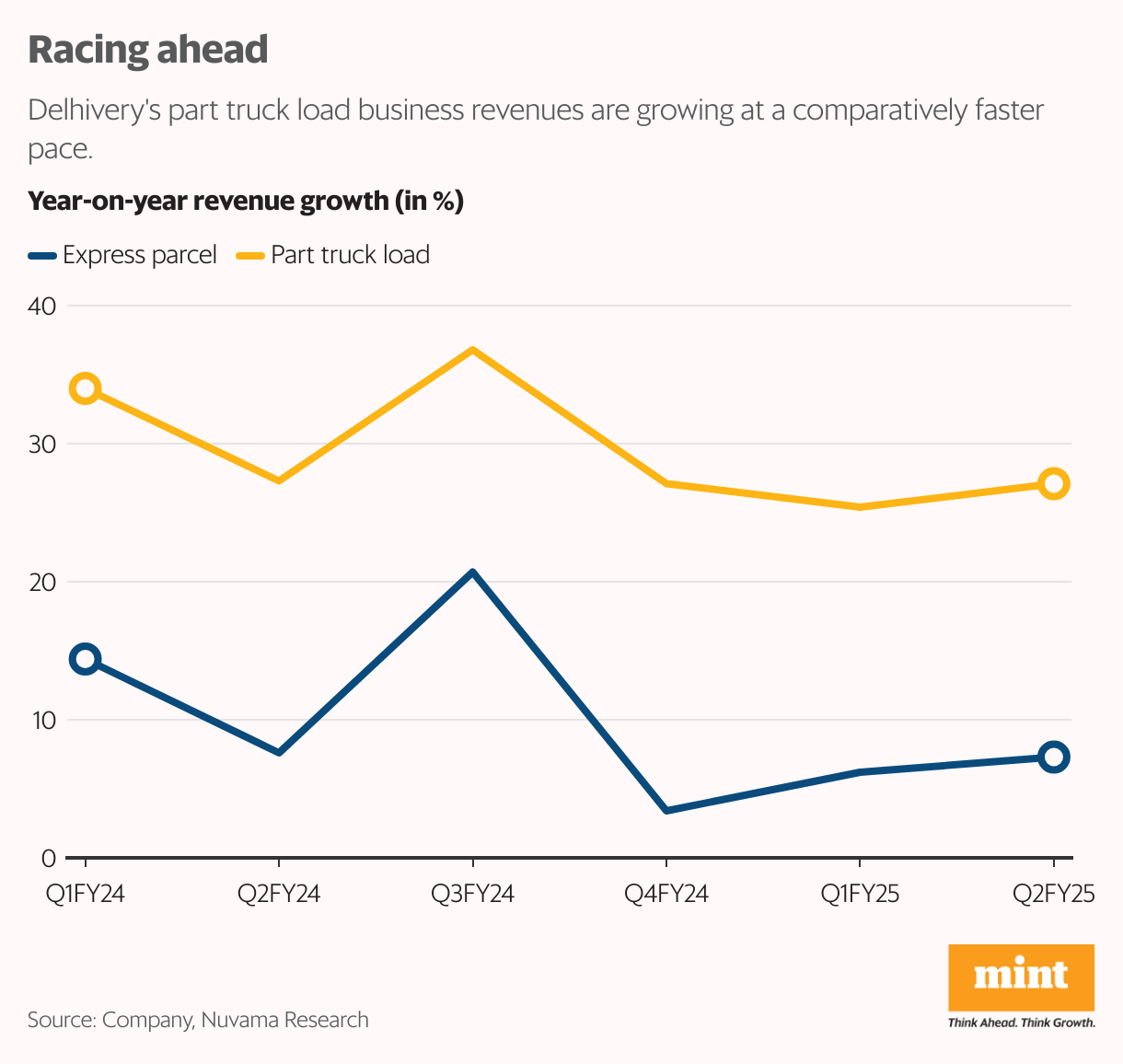

In Q2FY25, revenue from express parcels, contributing 59% of total revenue, was up 7%. In comparison, Delhivery’s part truck load (PTL) segment was the shining star, contributing 22% of total revenue and clocking 27% on-year growth led by a 23% volume growth and a 4% rise in realizations. Still, scaling costs and pre-season capacity investments hurt margins, which stood at 2.9% compared to 3.2% in Q1FY25 and negative in Q2FY24.

The future planning

Looking ahead, to boost growth, Delhivery is undertaking initiatives such as expanding a shared quick-commerce network for e-commerce, B2C, and B2B clients; introducing faster regional next-day surface shipping and national air shipping options; and rolling out an aggregator reseller franchise model akin to DTDC’s to cater to SMEs and D2C customers. Also, to fight quick-commerce competition, Delhivery is setting up facilities in 6-7 cities.

Delivery anticipates express parcel margin to be in the range of 15-18%. In the PTL segment, it is eyeing a sharp margin lift to 15-16%, riding on the back of scale, strategic price hikes, and operational synergies. “Improving PTL volumes without sacrificing realizations and benefits of operating an integrated network should aid the margin trajectory, in our view. Strong net cash position and reducing capex intensity (5% in FY26) is likely to help the company ward off industry headwinds better than competition,” said Emkay Global Financial Services.

For now, Delhivery needs demand to recover adequately and much also hinges on how competition shapes up. “While margins are likely to recover once the investments towards upgradation are over, we believe the current price point creates a reasonable level for entry,” said Nuvama Research.