And while the economy is galloping, there are pain points that are beginning to hurt. India has emerged as the fastest growing large economy with an enviable gross domestic product (GDP) growth of over 8%. However, the economic expansion has been uneven. The rural economy, particularly, has been sluggish and there simply aren’t enough jobs that pay well or are aspirational. The private sector, unsure of demand growth, is hesitant to invest. In fact, after the electoral outcome, there were worries of the Centre’s economic approach embracing populism.

The Union budget, presented on Tuesday, has eased many concerns. The government has stressed on fiscal consolidation, spending efficiency and capital expenditure (capex)-led growth.

Mint explains the budget’s many nuances and its potential long-term impact.

What were the concerns before the budget was presented?

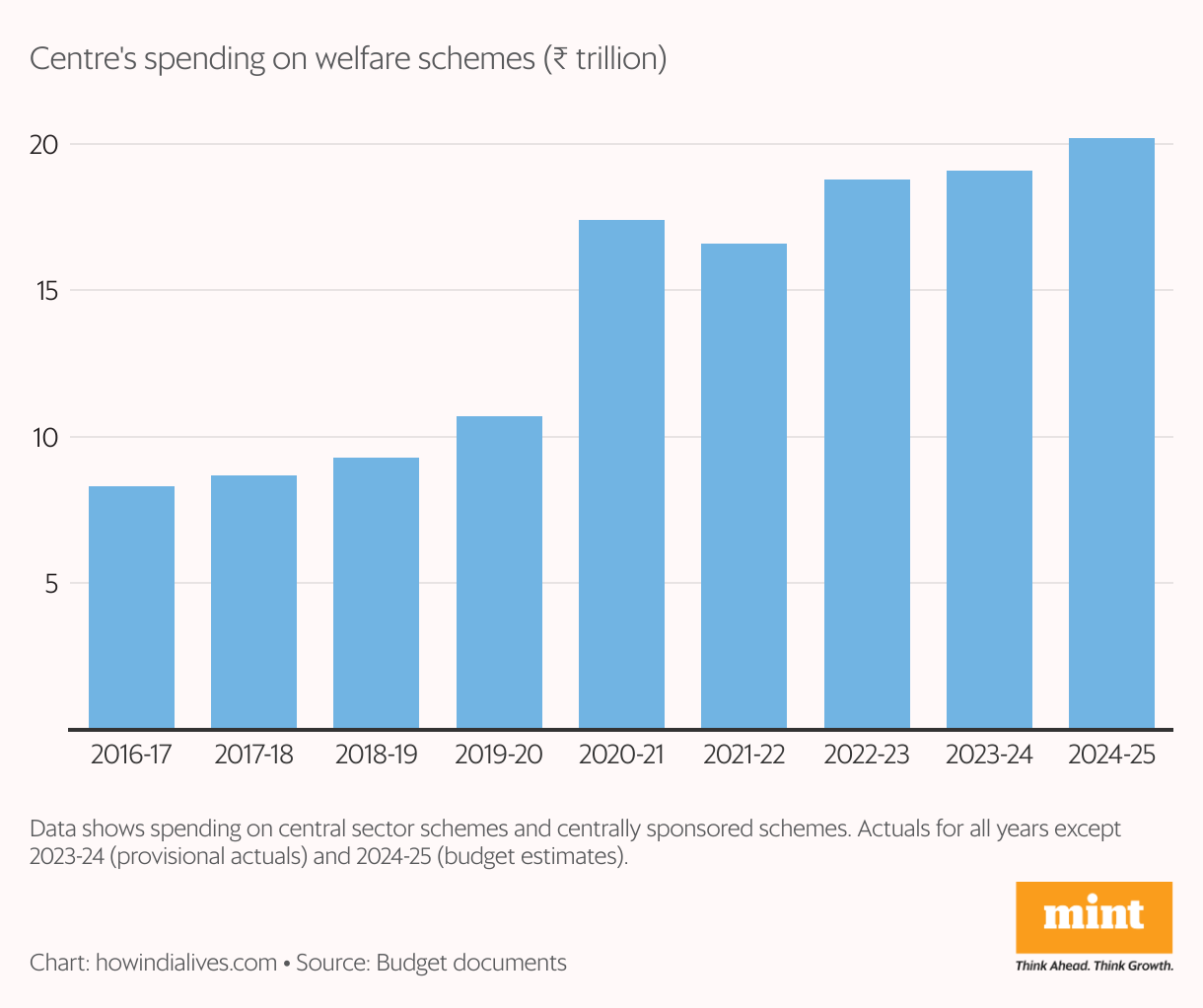

The biggest concern was whether the central government’s policy choices could change after the electoral outcome. Over the years, it had worked hard to improve spending efficiency by cutting back on revenue expenditure (expenses that are routine in nature like salaries and pensions) and focusing on capex (expenses that create assets) which had a greater multiplier effect. In the 2024-25 interim budget, the revenue expenditure as a share of the gross domestic product (GDP) had declined to 7.5%. In absolute terms, this was 4.5% lower than during the covid-19 period. Welfare and rural spending bore the brunt of the cuts.

The Bharatiya Janata Party (BJP)’s below par performance in rural seats during the general elections was partly blamed on these cuts.

This explained the fears—what if the government turned populist and splurged on welfare measures?

There were demands for a farm loan waiver, higher allocation for the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS), higher cash transfer under the PM KISAN scheme or even a new cash handout scheme.

Did people expect a capex rollback?

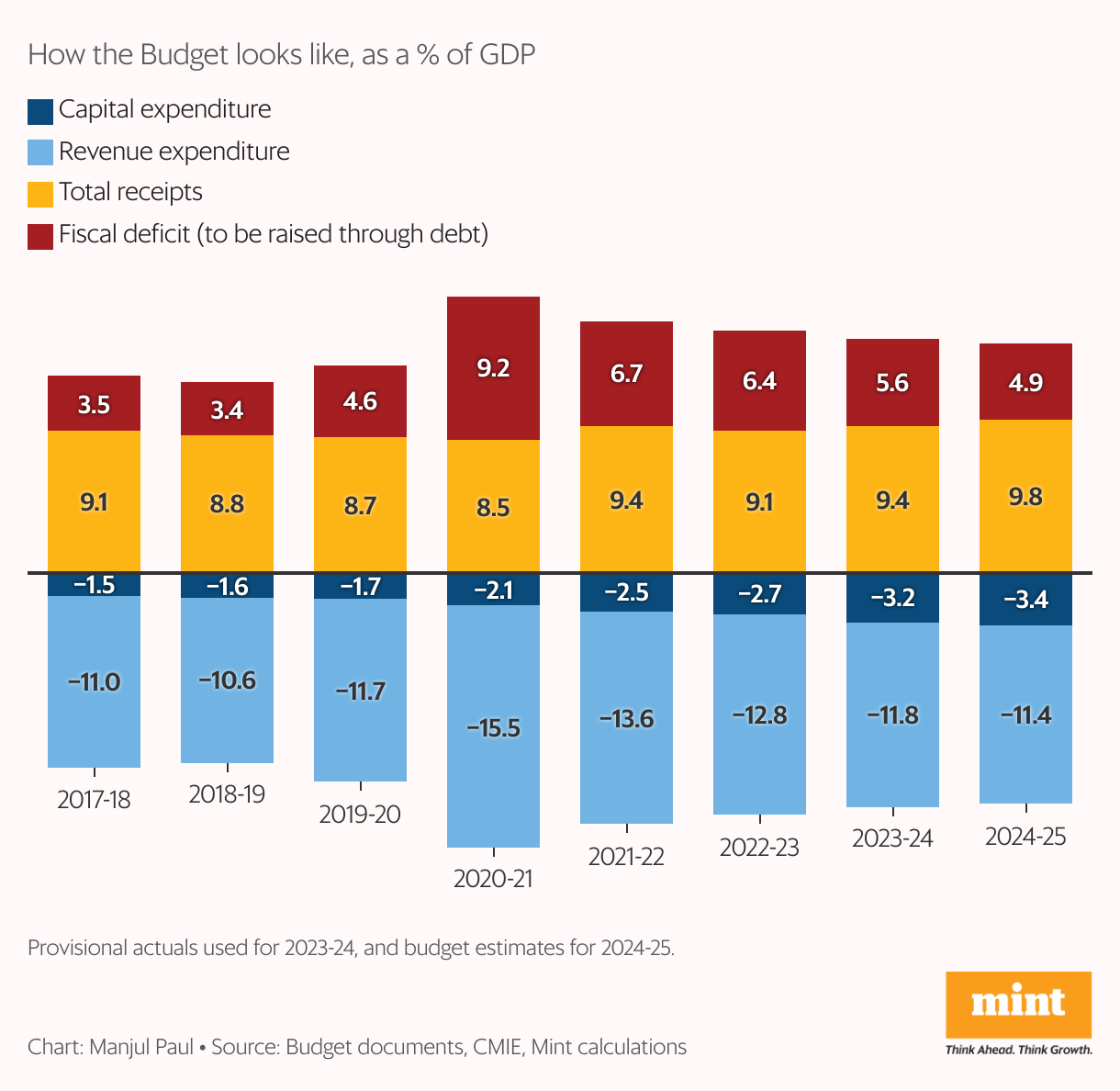

Some did. To generate resources for welfare spending, the government needed to inevitably scale back its capex spending. The last three years have seen a significant increase in capex as the government revved up public spending to drive growth in the hope that private investment will follow suit. It is this public spending that had powered India’s strong GDP growth. Also, populist spending would hurt the government’s fiscal consolidation record. The government has been steadfast in reducing the fiscal deficit (excess of government spending over its income) over the years and planned to reduce it to 4.5% by 2025-26 from the post-covid level of 9.2%.

The fear was that the government would slow down that glide path to create resources for welfare spending. These actions would have hurt India’s immediate growth and weakened the country’s long-term prospects.

How did the budget address these concerns?

The budget has sent a clear message that the electoral outcome has not forced a change in its economic thinking. Let us take the case of fiscal consolidation which many feared would slow down. In reality, the government has accelerated it.

The fiscal deficit for 2024-25 is expected at 4.9% of GDP as against 5.1% that was fixed in the interim budget presented in February. The government has committed that the fiscal deficit for 2025-26 would be below 4.5% and for every year post that, it would be such that the government’s debt is lower than the previous year.

The government’s net market borrowing at ₹11.63 trillion in 2024-25 would be lower than ₹11.75 trillion envisaged in the interim budget.

A lower fiscal deficit means less government borrowing from the market. This, in turn, would result in more funds being available for corporates and others to borrow at lower cost to fund their expansion. The government’s net market borrowing at ₹11.63 trillion in 2024-25 would be lower than ₹11.75 trillion envisaged in the interim budget.

Did the government spend more to address rural distress?

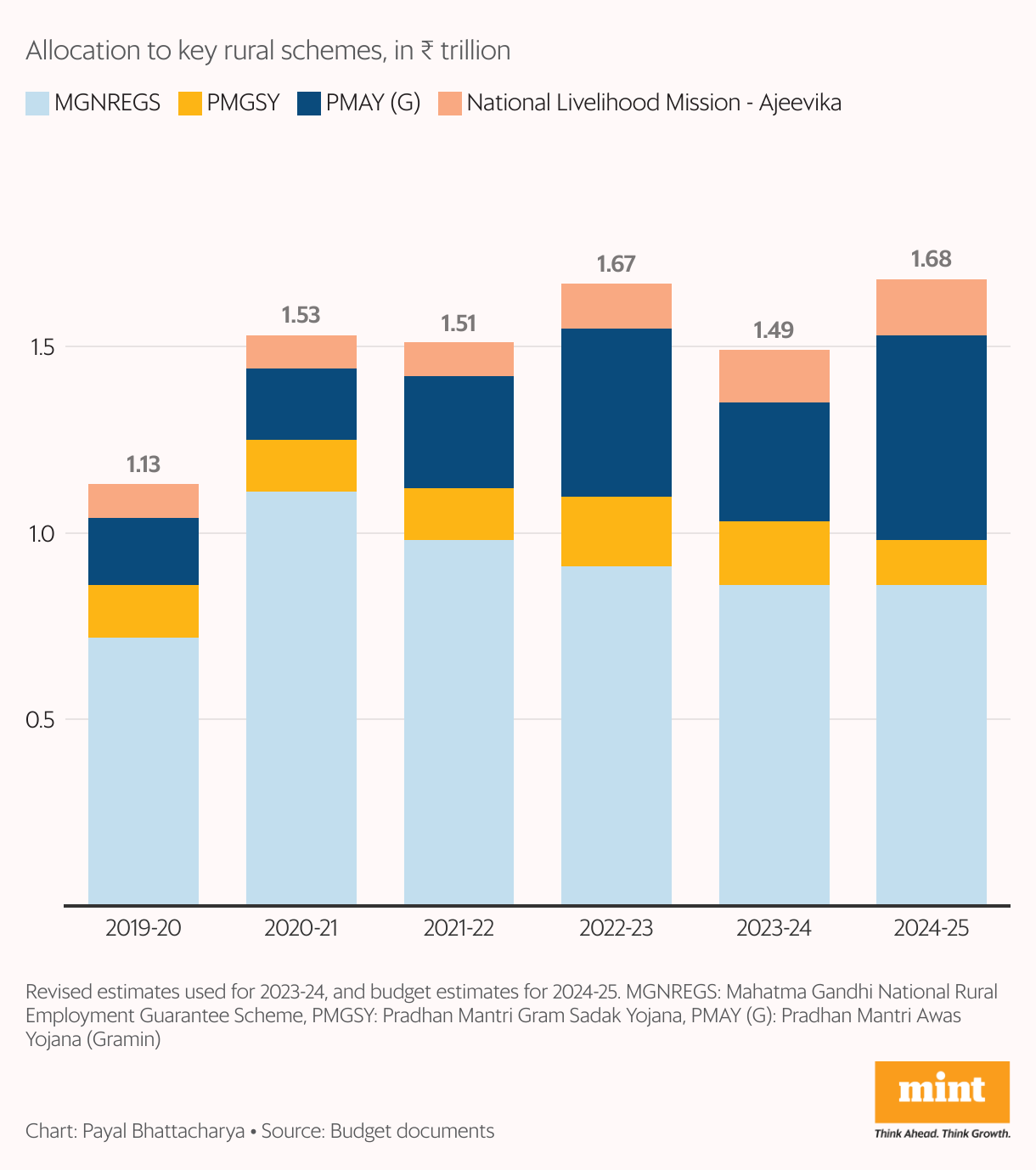

Yes, it did. Rural development received an allocation of ₹2.66 trillion. This includes ₹54,500 crore for affordable housing, a significant increase from ₹32,000 crore spent last year. As building houses is labour intensive, this could see substantial creation of rural jobs. Allocation for agriculture and allied sectors saw a modest increase in allocation of 6% from ₹1.31 trillion in 2023-24 (revised estimate) to ₹1.39 trillion in 2024-25. The focus is more on improving crop productivity and resilience to climate risk. For this, the finance minister seeks to reset the farm research system to release 109 high-yielding and climate resilient varieties of 32 crops. This move, if successful, will not only improve and protect farm income but also ensure stable prices for consumers.

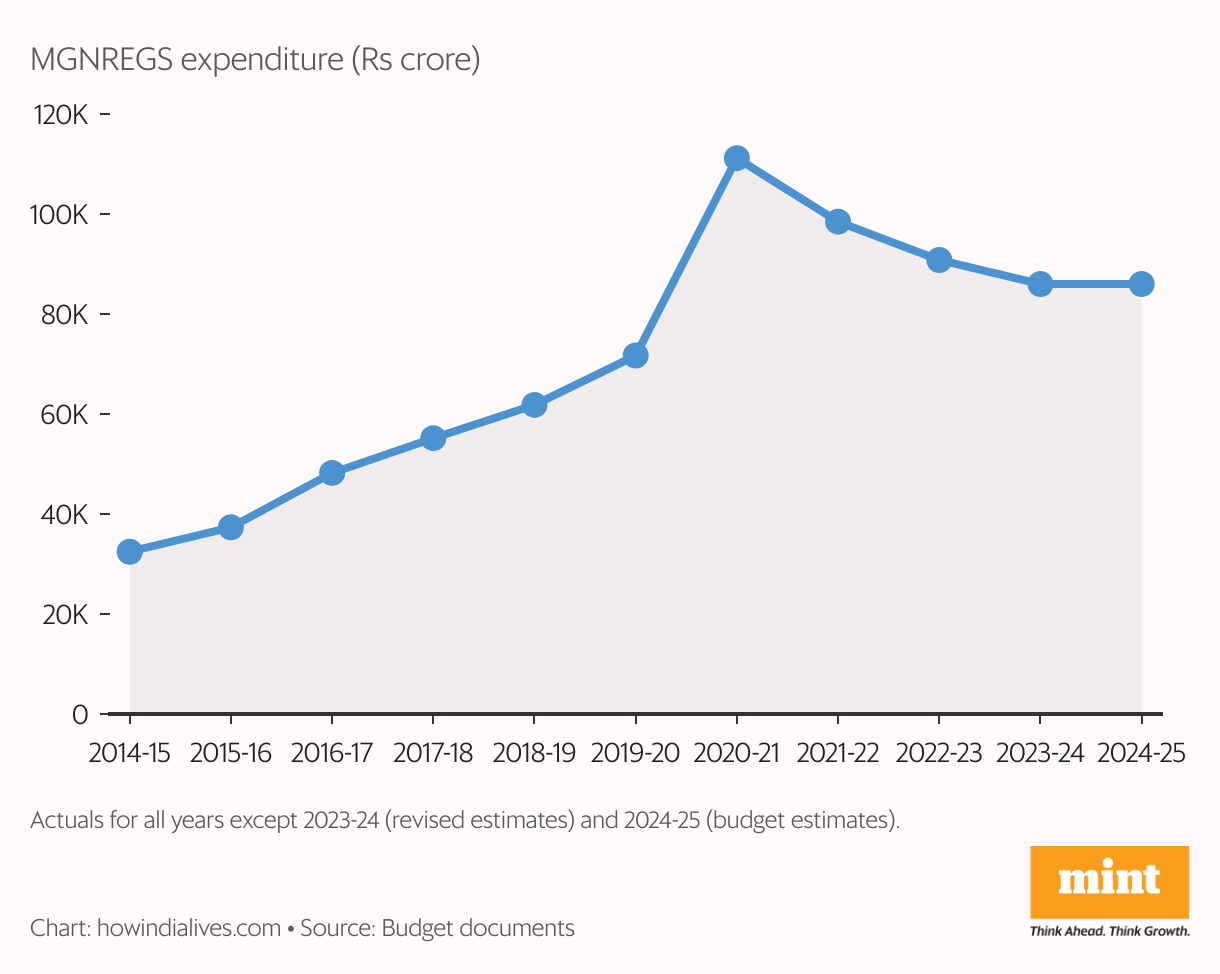

MNREGS allocation was ₹86,000 crore, same as the revised estimate of 2023-24. This could be based on past experience where demand for jobs under MGNRGS typically falls when the monsoon is good. Monsoon, this year, is expected to be normal. PM Kisan allocation also saw no increase.

What about jobs?

Creating adequate good quality jobs has become the biggest challenge for the government. Even though the economy is growing at a rapid clip, its job intensity (its ability to create jobs) is low. That needs immediate correction if India has to leverage its demographic advantage.

The government took up this challenge head on in this budget. It has come up with five schemes aimed at education, skilling and employment with an outlay of ₹2 trillion. In the next five years, these schemes will benefit 41 million youth. The outlay for this year is ₹1.48 trillion.

In the next five years, these schemes will benefit 41 million youth. The outlay for this year is ₹1.48 trillion.

These employment-based incentive schemes are the only new direct benefit transfer scheme announced in the budget. They will not only skill but also bring youth and women into the formal workforce. The success of this initiative will depend on close co-operation between the centre, state governments and industry.

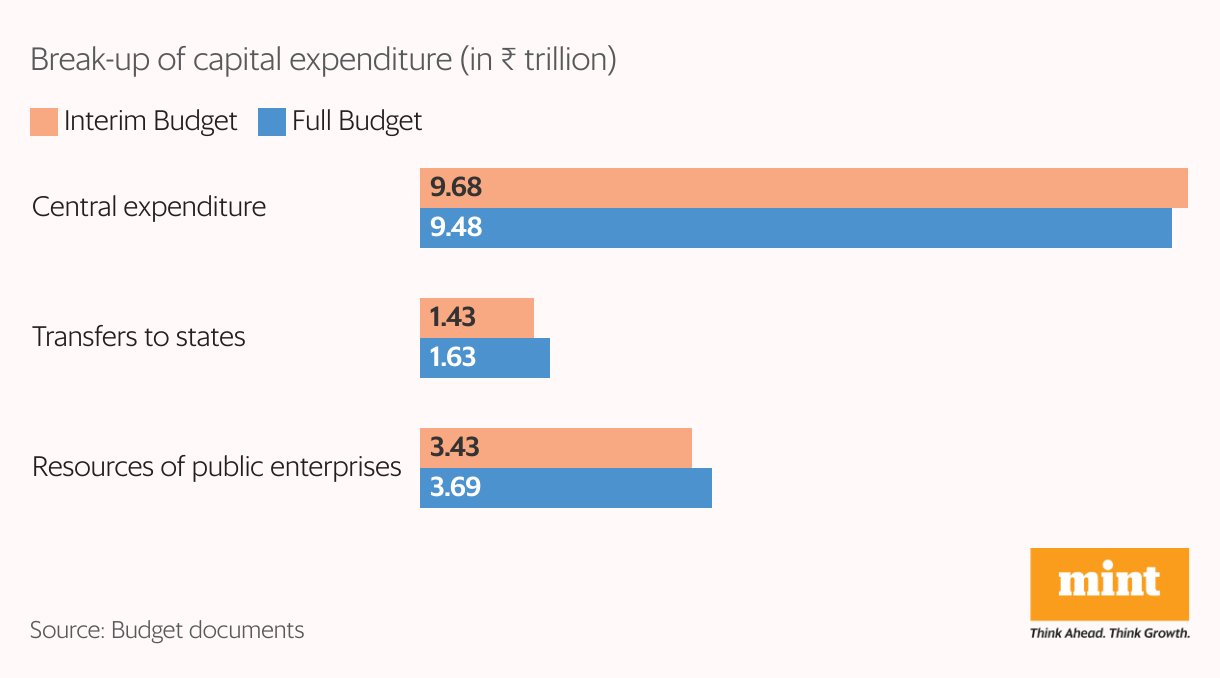

Has the capex focus continued?

Yes. The government has retained the capex outlay at ₹11.1 trillion as made in the interim budget. This works out to 3.4% of GDP. The capacity of the system to spend the allocated money would have played a part in not increasing the allocation further. According to Emkay Research, the capex spend has declined by 14% in the first two months of this fiscal and the spending in the rest of the months have to be significantly higher to meet the target. Also, the Centre is keen on pushing the states to spend more. It has increased the allocation for the 50-year interest free capex loan from ₹1.3 trillion to ₹1.5 trillion.

Experts have said that the capex spend of the states has less gestation period and is more labour intensive than that of the central government. So, the economic benefits accrue faster.

If spending is more and the deficit has reduced, how did the fiscal math work?

The budget math worked because the government got a dividend bonanza from the Reserve Bank of India amounting to ₹2.1 trillion—as much as 0.4% of the GDP. It used half of it (0.2%) to reduce the fiscal deficit and the other half to increase revenue allocations. The overall revenue expenditure, excluding interest payments, has risen to 7.8% of the GDP, up from 7.5% in the interim budget. The government also benefited from a 15% growth in projected revenue receipts. The budget has assumed a nominal growth rate of 10.5% but most experts expect it to be well over 11%. When it comes to resource mobilization, the government is well placed.

Did the government fall for a consumption stimulus?

To some extent. The increase in standard deduction and tweaking of the slab rates for those in the new income tax regime will leave ₹17,500 in the hands of the salaried employee.

The big question is if this money will be spent or saved. One of the main reasons why the government has stayed away from any stimulus to boost consumption is that its multiplier effect—the cascading benefit that the economy gets—is far lesser than spending by the government. The latest move must be seen more as an effort to provide relief for the salaried class, especially the middle class, and not as an attempt to boost consumption.

Sluggish private investment remains a challenge. What plans did the budget have?

A lot has already been done to cajole the private sector to drop its reticence and invest. The government has been spending heavily ( ₹28.11 trillion between 2022-23 and 2024-25 on capex) hoping that it will pump prime private investment (or investment made by private industries).

A study by Mint of India Inc’s cash flow shows that the industry’s net cash from operation has surged 26.4% in 2023-24.

It has come up with a production-linked incentive scheme (it has attracted investments worth ₹1.28 trillion as of May 2024 as per the Economic Survey) and most importantly, cut corporate tax rates significantly.

A study by Mint of India Inc’s cash flow shows that the industry’s net cash from operation has surged 26.4% in 2023-24. This clearly means that capacity utilization is high. But a study of the investments the same companies made in fixed assets shows that it has risen by only 10.7%, the slowest post-pandemic growth.

The government is hoping that the long overdue investment cycle will pick up this year.

What measures did the budget propose to revive the informal sector?

View Full Image

A recent study by India Ratings and Research revealed that between 2015-16 and 2022-23, as many as 6.3 million unincorporated enterprises shut down and 16 million jobs were lost. These informal enterprises typically create more jobs as the industry is more focused on profits and drives productivity in a big way. Understanding the importance of medium, small and micro enterprises (MSMEs), the budget rolled out multiple initiatives to ease funding, which is the biggest bugbear for them. A new credit guarantee scheme will be in place to enable manufacturing MSMEs to raise funds for procuring plant and machinery without a need for collateral. This will help them to expand and gain scale. The limit for Mudra loans has been doubled for those entrepreneurs who had availed these loans and paid them back.

According to a study, between 2015-16 and 2022-23, as many as 6.3 million unincorporated enterprises shut down and 16 million jobs were lost.

Also, a new mechanism has been announced to fund MSMEs which are under stress and classified as a ‘special mention account’. Hitherto, they received no funding, and they inevitably became a non-performing asset. In addition, the finance minister announced measures that can help MSMEs improve their cash flow.

Equity investors aren’t that happy. Why?

The budget has increased the capital gains tax—both short and long term. This came as a shock to investors. The finance minister has said that it has been done to simplify the levy. Short-term capital gains will now be taxed at 20% instead of 15% while long-term capital gains will be taxed at 12.5%, up from 10%.

The indexation benefit that was hitherto available has been removed for all asset class including real estate. The securities transaction tax on futures and options trading has been increased sharply as volumes in this segment have reached alarmingly high levels. Expectedly, the market didn’t like these provisions.

View Full Image

In short, can one call it a balanced budget?

It is. The budget has maintained the focus on fiscal consolidation without compromising on the need to spend on areas that need support. The fiscal deficit in the budget proposal has been reduced even as revenue expenditure has risen. The overall quality of spending is not being compromised. The finance minister has also balanced the immediate needs of the economy while investing in the future—in areas such as agricultural research, human capital development and space.